The increase was announced in the Minister of Finance’s Budget Speech on 21 February 2018. The standard rate of VAT will change from 14% to 15% on 1 April 2018 (the effective date).

How will this VAT increase affect property transactions, property registrations and estate agent commissions?

Question 1: How will the rate increase work generally for fixed property transactions?

The rate of VAT for fixed property transactions will be the rate that applies on the date of registration of transfer of the property in a Deeds Registry, or the date that any payment of the purchase price is made to the seller – whichever event occurs first. (See, however, the exception in Question 2 below where registration (delivery) of the fixed property occurs on or before 23 April 2018.)

If a “deposit” is paid and held in trust by the transferring attorney, this payment will not trigger the time of supply as it is not regarded as payment of the purchase price at that point in time. Normally the sale price of a property is paid to the seller in full by the purchaser’s bank (for example, if a bond is granted) or by the purchaser’s transferring attorney.

However, if the seller allows the purchaser to pay the purchase price off over a period of time, the output tax and input tax of the parties is calculated by multiplying the tax fraction at the original time of supply by the amount of each subsequent payment, as and when those payments are made. In other words, if the time of supply was triggered before 1 April 2018, your agreed payments to the seller over time will not increase because of the increase in the VAT rate on 1 April 2018.

Example:

A vendor sells a commercial building and issues a tax invoice to the purchaser on 10 January 2018. If the property will only be registered in the Deeds Registry on or after 1 April 2018 and payment will be made by the purchaser’s bank or transferring attorneys on the same date, then the time of supply will only be triggered at that later date. In this case, VAT must be charged at 15% as the rate increased on 1 April 2018 which would be before the time of supply. It does not matter that an invoice or a tax invoice was issued before the time of supply and before the VAT rate increased. The tax invoice in this case would also have to be corrected as it would have indicated VAT charged at the incorrect rate of 14%.

See also the next questions below for the rate specific rule that provides an exception for the purchase of “residential property” or land on which a dwelling is included as part of the deal.

Question 2: Is there a rate specific rule which is applicable to me if I signed the contract to buy residential property (for example, a dwelling) before the rate of VAT increased, but payment of the purchase price and registration will only take place on or after 1 April 2018?

Yes. You will pay VAT based on the rate that applied before the increase on 1 April 2018 (that is 14% VAT and not 15% VAT). This rate specific rule overrides the rules as discussed in Question 1, which applies for non- residential fixed property.

This rate specific rule applies only if:

- you entered into a written agreement to buy the dwelling (that is “residential property”) before 1 April 2018;

- both the payment of the purchase price and the registration of the property in your name will only occur on or after 1 April 2018; and

- the VAT-inclusive purchase price was determined and stated as such in the agreement.

For purposes of this rule, “residential property” includes:

- an existing dwelling, together with the land on which it is erected, or any other real rights associated with that property;

- so-called plot-and-plan deals where the land is bought together with a building package for a dwelling to be erected on the land; or

- the construction of a new dwelling by any vendor carrying on a construction business;

- a share in a share block company which confers a right to or an interest in the use of a dwelling.

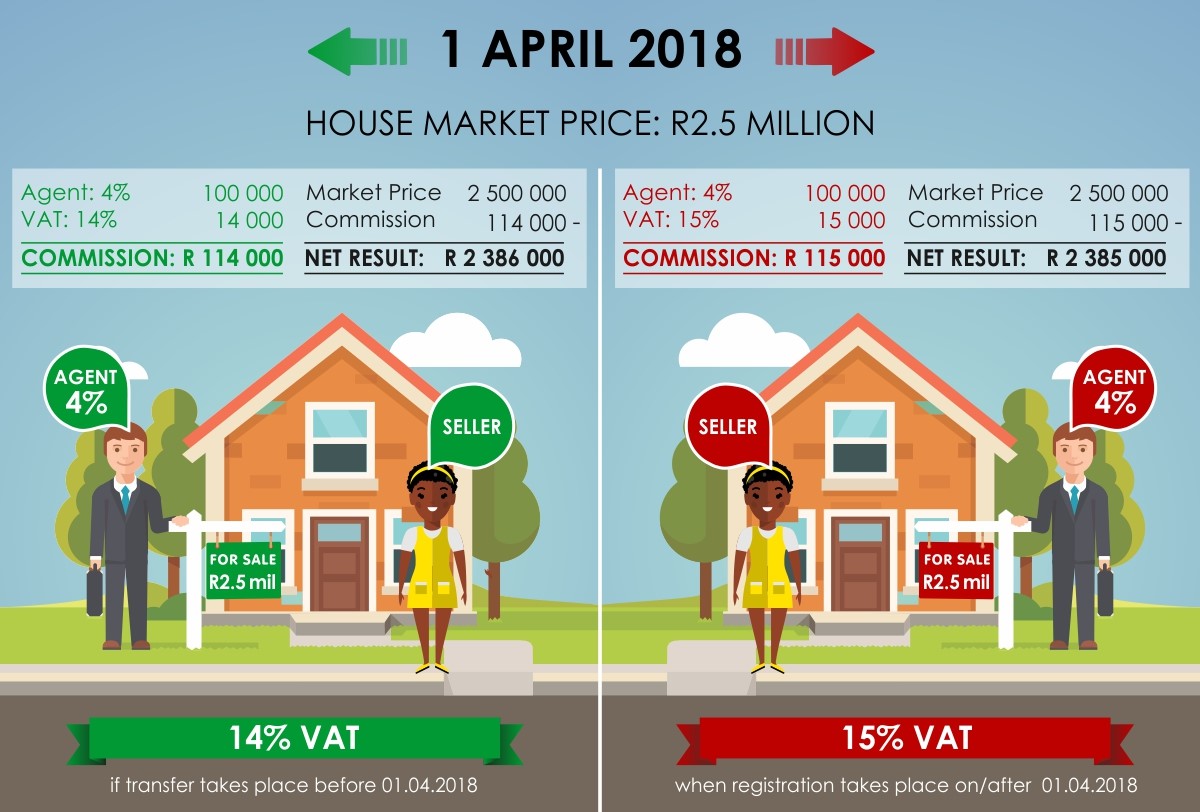

Question 3: How will the VAT increase affect the seller of the property and estate agent commission?

Two possible scenarios can apply:

Scenario 1:

Should the contract of sale read that a percentage commission plus VAT is payable, that will be calculated at 14% if transfer takes place before 1 April 2018 and at 15% when registration takes place on or after 1 April 2018.

The net result is that the seller (who sold prior to 31 March 2018) will receive a lower net amount on the selling price because of the increased VAT, should transfer take place after 31 March 2018.

Scenario 2:

Should the contract of sale refer to a fixed commission amount inclusive of VAT, the opposite will apply. The seller will receive the same amount, but the agent will receive less because of the increased VAT.

For more information on the VAT Increase, download the SARS VAT Increase general guide and FAQs here:

Please contact us should you have any specific questions.

This article is a general information sheet and should not be used or relied on as legal or other professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your legal adviser for specific and detailed advice. Errors and omissions excepted (E&OE)